Several years ago, our financial advisor and good friend began talking to us about retirement planning, college savings for our infant daughter, and the importance of life insurance. He said, “It’s not cheap, but you need to do it.” He advised us on the company to choose, began the paperwork, and told us how to continue the application process. Of course, I didn’t look forward to taking on the cost or the administrivia of applying for life insurance. “You’ll need to answer questions about your income and health and have physicals,” our friend told us. Nevertheless, there was something oddly fulfilling about applying. Life insurance isn’t a fun topic or process, but it represented a milestone in our lives. With a family, I was ready to think about someone other than myself.

The Emotional Side of Life Insurance

The woman processing our application was perfectly nice and professional. Some of the questions she asked caused some anxiety and made me feel defensive—those about drinking and exercise. Others, I answered proudly—no smoking, good eating. However, I wasn’t prepared for one question: “Are your parents alive or deceased?” My dad had passed away a few months earlier. I felt my renowned ability to contain my emotions start to waiver. She expressed her sympathy and asked the reason. I answered, “pancreatic cancer,” and started crying, then apologized, saying it was still recent so I hadn’t gotten used to talking about it. She was very patient, then we continued with the questions.

Champion Advertisement

Continue Reading…

Purchasing life insurance involves some cold elements such as policies, premiums, risk, and assets; but for customers, the process can be very personal and emotional. The driving concept behind life insurance—your loved ones’ security—and a variety of potential emotions—whether mourning a deceased parent or reflecting on one’s own health and lifestyle—make the process of buying life insurance more emotionally charged than most people would assume. Plus, the emotions that are inherent in seeking life insurance are in direct conflict with the very transactional nature of the process of applying for it.

With this conflict and various hurdles such as the need for a physical, the complexity of the available types of coverage, the paperwork, and the cost, it’s not surprising that many people fail to complete the application process and never purchase a policy. Even though some people do become policyholders, lapsing policies have significant negative impacts on the revenue and growth of life-insurance companies.

Most policyholders believe, when purchasing life insurance, they can just set it and forget it. Once I had purchased my life insurance, I thought, now I just wait to die. Life-insurance companies—who do little more than send premium-payment reminders and administrative updates—do nothing to change that erroneous perception. Therefore, it’s not surprising that customers let their policies lapse. Most insurance companies have done little to remind policyholders about the service they provide, let alone to ensure their satisfaction, engagement, and loyalty.

Reinventing Life Insurance

The issues customers have with legacy insurance companies translate to opportunities for new insurance companies to serve people who have never had life insurance or whose policies have lapsed. As a consequence, new insurance technologies, or insurtech, are transforming the insurance industry by improving customer satisfaction, reducing costs for both customers and insurance companies, and improving efficiency. Insurtech companies are making the process of researching and comparing policies and purchasing life insurance easier and more convenient.

In fact, Insurtech disruptors are capturing some of the $16 trillion in lost revenues from customers that the Life Insurance and Market Research Association (LIMRA) has identified as “stuck shoppers,” who don’t complete the quoting process. [1, 2] Companies such as Ladders tout their services’ simplicity and ease of use and are eliminating the complexity of purchasing a policy. Plus, banks and financial institutions are increasingly leveraging their relationships with existing customers by expanding their services to include annuities. Because of these competitive forces, life-insurance companies are now trying to do a better job of engaging with their policyholders.

Many insurance companies are pursuing digital-transformation efforts in the hope that designing Amazon-like portals and mobile apps that offer self-service would create more loyal customers. I’m sorry to say that they do not. Building a portal and expecting proactive policyholders to visit it, giving you the opportunity to upsell or cross-sell to them, is a pipe dream. Why? Because life insurance isn’t part of people’s daily lives. Their mental model is: I set up the policy. I pay the premiums. I die.

Maybe, when customers need to make changes such as updating their beneficiaries or changing their address, they’ll think about visiting a portal, which can be valuable for handling such service tasks. But a cross-sell or upsell offer is not likely to persuade policyholders who are visiting a portal to make a quick change. They simply don’t have the kind of relationship with their life-insurance company that would prompt them to consider such offers. Especially not when the cold, transactional experiences that these companies have created have trained these customers not to expect a positive relationship with their insurance company. However, life-insurance companies can improve their relationships with customers—not through portals or mobile apps, but by acknowledging how people perceive life insurance today, reinventing the way they do business, and adopting a people-centered approach to service.

Life Insurance and the Purchasing Decision

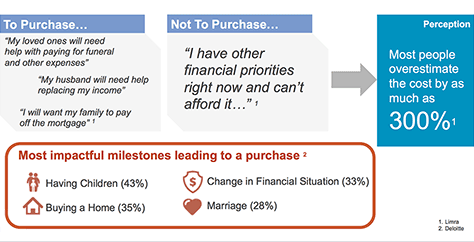

Purchasing life insurance seems like a no-brainer, so why don’t more people do it? There are both hard and soft reasons for making the decision to purchase or not to purchase, as illustrated in Figure 1. For example, most people believe that life insurance is more expensive than it is—overestimating the cost by 300%—and many people have competing financial priorities. [3] But there are also softer concerns that influence people’s perception about buying life insurance, as follows:

Does the purchasing decision stir up positive or negative emotions?

Are the outcomes of the decision tangible or nebulous?

Are the outcomes immediate or long term?

Is the decision simple or complex?

Figure 1—Purchasing decision

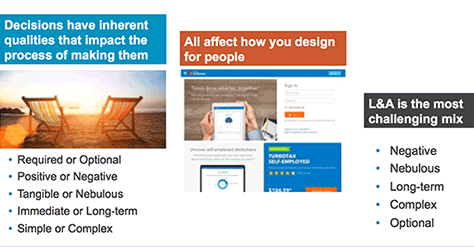

Figure 2 shows that decisions around purchasing life insurance are the most challenging mix of the above concerns: life insurance can stir up negative emotions because of its focus on death and the complexity of the products and services, whose benefits are intangible and long term.

Figure 2—Decision-making qualities

But family or loved ones’ security is at the core of this purchasing decision. Because the purchasing journey is complicated, you can see why creating an Amazon-like customer portal wouldn’t be a silver-bullet solution. Instead, insurance providers need to begin changing the core perceptions that influence people’s decision-making and reinforce the characteristics that are opposite to what people think about life insurance today: simplicity, tangibility, positivity, and immediacy.

Let’s look at the policy-application process as an example: During a review of 13 large life-insurance companies’ online application forms and the 269 questions that they collectively asked prospects, researchers found the following:

90% of the questions focused on coverage requirements, medical and health assessments, administrative details about beneficiaries, and financials and assets.

7% of the questions asked about the policyholder’s future, including questions about burial costs.

Only 3% of the questions—or eight questions in total—were positive or goal focused in nature, focusing on the prospect’s future needs.

Therefore, during the application process, one of the first critical milestones in the customer’s service experience, these life-insurance companies focused predominantly on gathering information that would help them evaluate risk and set a policy price. The tone of these questions simply reinforces people’s negative perceptions of life-insurance companies. The questions were:

negative—Do you smoke? What are your funeral needs?

complex—What coverage do you want?

offered little value—There was minimal discussion about the benefits of the policy, so few reminders of their reasons for applying.

As a prospect, what this line of questioning says to me is that the company cares more about their own risk than helping me protect my family. These questions also communicate that the company doesn’t care about the fact that I’m trying to be healthier or might be concerned about what kind of policy I can afford. These questions simply reinforce the one-sided, transactional nature of life insurance and do not reflect the very human and emotional attributes of life insurance. Such questions do not attempt to invert customer attitudes about life insurance—simple versus complex or positive versus negative—or communicate the obvious benefits of having a life-insurance policy.

Reimagining Policyholder Relationships by Acting as an Advisor on Life

The life-insurance business model is ripe for re-invention. If insurance companies are to remain competitive in the evolving insurtech market, strategic service design that reimagines the insurance company’s relationship with policyholders is key to that re-invention. Life-insurance companies should function as advisors on life, not just life insurance.

Focus on the Life That’s in Between

A life transpires between a policy’s inception and a policyholder’s retirement or death. That life might include kids, college financing, health improvements and declines, salary shifts, second homes, or caretaking of parents or grandparents. Policyholders’ definition of security inevitably evolves, so all of these life milestones are potential touchpoints for reassessing a policyholder’s needs and determining potential upsell and cross-sell opportunities.

Redefine Who Customers Are

While policyholders usually pay the premiums, the insurance company’s customers also include the beneficiaries—who are just as important as the policyholders because they’re the ones who motivated the policyholders to do business with the company in the first place. When insurance companies think about how best to communicate with policyholders, they also need to consider the broader system of influencers and loved ones who are important to them and understand their goals and needs.

Only when life-insurance providers truly serve families in both life and in death have they developed the kind of relationship in which customers might engage with cross-sell and up-sell opportunities. They’ve also created loyal families and a pipeline of future policyholders. According to LIMRA, claimants who are extremely satisfied with a claims process are four times as likely to do business with the company themselves, in comparison to claimants who are merely satisfied with the process. [4]

Create an Advisory Service

Not everyone can afford to hire a financial advisor or wealth manager. The underserved life-insurance customer constitutes the largest market segment, and these customers need guidance to find the right policy. Life-insurance providers could play a valuable role in helping people understand what’s right for their family, what others do in similar situations, and what value and security they’ll get in exchange for their payments.

The goal of reimagining the insurance provider’s role and relationship with customers is to change their perceptions about life insurance. Adopting a people-centered customer-engagement model ensures a company’s decisions regarding business, technology, process, and communication support this goal.

Shifting to a New Customer-Engagement Model

Professionals in UX and service design understand that people-centered design methods can help insurance companies better understand their customers and their interactions with them, allowing them to engage with customers in more meaningful ways. For many life-insurance providers, the development of a customer-centered mindset is less mature than at companies in many other domains. Therefore, insurance companies need guidance on where to begin. Here is my advice on the steps insurance companies should take to transform the way they do business with their customers:

Develop personas for prospects, policyholders, beneficiaries, and agents. Many insurance companies already have policyholder and prospect profiles, but they should also develop personas for agents and beneficiaries. Remember, the goal is to illustrate a holistic representation of the life-insurance journey for all personas, not just the policyholder who pays for the policy.

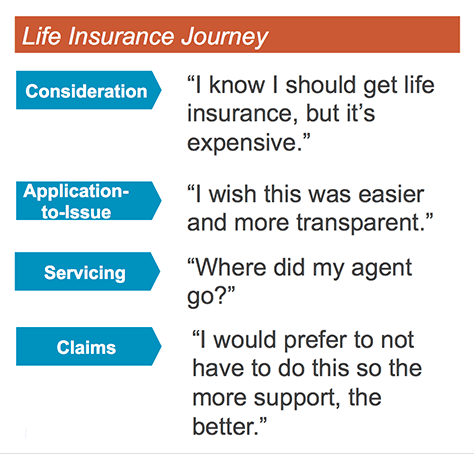

Create journey maps and touchpoint maps. Use these to determine customers’ painpoints, service gaps, and opportunities to improve the insurance experience. Figure 3 shows a symbolic journey map. Maps of customer journeys and touchpoints

connect customer-experience key performance indicators (KPIs) to business metrics—It’s easy to trace hard metrics such as quotes, written policies, and renewals to the indicators of a positive customer experience. Journey maps should reflect this relationship between business impact and customer experience.

should be living, breathing project documentation—It’s necessary to evaluate and iterate them over time, not just create them once when designing a portal, then leave them on a shelf.

should be based on the insurance company’s actual customers—There is no such thing as a generic life-insurance customer.

reflect the actual experiences of customers and agents—Employee behavior relates directly to the customer experience, so insurance providers should document and understand both.

incorporate input from internal stakeholder workshops—The purpose of these workshops is to elucidate internal processes and technologies that impact the employee experience.

start small with a particular use case—Over time, expand these use cases to represent the life experience of policyholders and their families or beneficiaries. Developing use cases helps stakeholders to discover touchpoint opportunities that connect their milestones to the insurance company’s products and services.

Research how the insurance company communicates with both prospects and policyholders. Determine how to streamline and enhance cross-channel touchpoints, including customer support, insurance agents, mailings, email messages, and Web sites. Once you’ve documented the customer journey, aggregate all of the relevant communications and post them on a wall. Begin walking through these materials, keeping the customer personas top of mind, and ask:

Does this communication make sense given where it occurs during the customer journey?

What does it communicate? Is the tone representative of the company’s goals of simplicity, tangibility, positivity, and immediacy?

Does it represent the new model of customer engagement: serving as an advisor on life for the family?

Does it address painpoints and barriers across the journey?

Review the data on policyholders and their families. Tap into social-media channels and other publicly accessible data to gain new information about policyholders and their beneficiaries.

Define an analytics and data strategy. Address gaps in understanding, focusing on the new model of customer engagement.

Explore investment in technologies and process improvements. Providing better support to employees enables them to interact with customers in new ways. If you fully embrace customer service for the life that’s in between, IoT and wearables can play a role in health monitoring just as they do for the health-insurance industry. Moreover, product accelerators allow reduced speed-to-market for new, truly customer-centered products that enable agents to interact with prospects in real time.

Figure 3—High-level journey

The goal should be to change people’s perceptions about life insurance. The customer’s decision to engage with an insurance provider should be simple, tangible, immediate, and positive. Adopting a people-centered customer-engagement model ensures that an insurance company makes business, technology, process, and communication decisions that support this goal. Moreover, by gaining a better, more holistic understanding of prospects, policyholders, and their loved ones, insurance providers can serve them more effectively and build a trusted, advisory relationship that presents more cross-sell and upsell opportunities and fosters customer loyalty.

Service Design and Business Impact

Service design provides a great example of how UX design professionals can have broader, more strategic impact through the experiences they design. By practicing service design, you can create new customer-engagement models and define new services, as this life-insurance example has shown.

Conduct business-oriented discussions with stakeholders that connect to what they care about—for example, growth, revenue, or efficiency. But always place the customer and employee experience at the center of the service.

Savvy UX-design professionals are adept at functioning as the fulcrum between business and information technology (IT), leading discussions about the goals for an experience and tying these goals to design execution. With service design, you’re simply expanding your expertise to mapping these business goals to the service experience that can deliver the desired outcomes.

Thanks for this good read. In my opinion it’s not just something Life Insurance companies could benefit from but also health or car insurance companies. However, they tend to have more customer interactions during the insurance lifetime.

The part where companies just launch new portals and/or apps and then think the customers just magically turn up is sadly true. Starting with a better mix of using “hard” KPIs and “soft” customer experience key performance indicators can help. Also I do wonder how much of AI could handle the more unpleasant “90%” of the more or less it’s all about us type of questions. It might soften the process and provide a better overall customer experience by just being able to focus on the actual customer side.

I agree about the mix of hard and soft metrics. We had a project with a small commercial insurance company who wanted a VOC program (voice of the customer). We mapped the high-level journey, similar to the one in this article, and had them outline the core business goals (policy purchase, etc.). We then brainstormed drivers of the ideal experience, and it was things like Trust, Ease, Desirability, and Value Beyond the Product. These were softer drivers that we then attributed measurable KPIs to (e.g., policy application drop-off). It helped connect harder business outcomes to softer CX considerations.

Wow, this is an interesting and informative post. Keep it up! The article “Insurance Website Design” will also be interesting to read on this topic. It covers the main points in creating an insurance website design, which also includes examples of successfully created insurance website designs.

Director of Strategy & Experience Design at NTT Data

Woodbridge, New Jersey, USA

Laura’s 10 years of experience have focused on representing the human element in any interaction with a brand through actionable, business-impacting insight gathering and design. At NTT Data, Laura leads cross-channel experience design strategy engagements for clients. Clients have included AstraZeneca, Hachette Book Group, GlaxoSmithKline, Prostate Cancer Foundation, Honeywell, and the NBA. In addition to her Service Design column for UXmatters, Laura has written articles for the Service Design Network’s Touchpoint: The Journal of Service Design, User Experience Magazine, Communication Arts, and Johnny Holland. She has presented on service design at SDN’s Global Service Design Conference, the Usability Professionals’ Association International Conference, IxDA New York City, and IxDA New Jersey. Read More